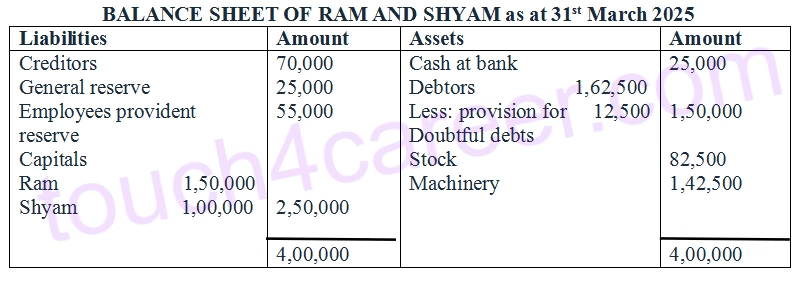

77 :- On 31st March, 2024, the balance sheet of Ram and Shyam who share profits and losses in the ratio of 3:2 was as follows

They decided to admit Mahesh on 1st April 2024, for 1/5th share which Mahesh acquired wholly from Shyam on the following terms:

(i) Mahesh shall bring Rs 25,000 as his share of premium for goodwill.

(ii) A debtor whose dues of Rs 7,500 were written off as bad debts paid Rs 5,,000 in settlement.

(iii) A claim of Rs 12,500 on account of workmen compensation was to be provided for.

(iv) Machinery was undervalued by Rs 5,000. Stock was valued 10% more than its market value.

(v) Mahesh was to bring in capital equal to 20% of the combined capitals of Ram and Shyam after all adjustments.

Prepare revaluation account, partners capital accounts and balance sheet of the new firm.

78 :- Aan and Shaan were partners sharing profits in the ratio of 3:2. Their balance sheet as at 31st March, 2024 was

They agreed to admit Mohan for 1/4th share on the above date subject to the following terms

(i) Mohan to bring in capital equal to 1/4th of the capital of Aan and Shaan after all Adjustments including premium for goodwill.

(ii) Building to be appreciated by 20% and stock to be depreciated to 70%

(iii) Provision for doubtful debts on debtors to be raised to Rs 10,000

(iv) A provision be made for Rs 18,000 for outstanding legal charges.

(v) Mohan’s share of goodwill premium was calculated as Rs 1,00,000

Prepare revaluation account, partners capital accounts and the balance sheet of the new firm.

Question 1 to 5 (Calculation of New Profit – Sharing Ratio and Sacrificing Ratio)

Question 6 to 10 (Calculation of New Profit – Sharing Ratio and Sacrificing Ratio)

Question 11 to 14 (Calculation of New Profit – Sharing Ratio and Sacrificing Ratio)

Question 15 to 18 (Calculation of New Profit – Sharing Ratio and Sacrificing Ratio)

Question 19 to 23 (Goodwill/Premium for Goodwill is brought in Cash by the New Partner and Retained in the Business)

Question 24 to 28 (Goodwill/Premium for Goodwill is brought in Cash by the New Partner and Retained in the Business)

Question 29 (Premium for Goodwill brought in Kind)

Question 30 to 32 (When Premium for Goodwill is brought by New or Incoming Partner and is withdrawn by Old Partners Fully or Partly)

Question 33 to 34 (When Only Part of Premium for Goodwill is brought by New Partner)

Question 35 to 36 (When New or Incoming Partner is not able to bring his Share of Premium for Goodwill)

Question 37 to 41 (Hidden Goodwill)

Question 42 to 46 (Revaluation of Assets and Reassessment of Liabilities)

Question 47 to 50 (Revaluation of Assets and Reassessment of Liabilities)

Question 51 to 54 (Reserves and Accumulated Profits/Losses and Preparation of Revaluation Account)

Question 55 to 56 (Preparation of Revaluation Account and Partner’s Capital Accounts)

Question 57 to 60 (Preparation of Revaluation Account, Partner’s Capital Accounts and Balance Sheet)

Question 61 to 64 (Preparation of Revaluation Account, Partner’s Capital Accounts and Balance Sheet)

Question 65 to 68 (Preparation of Revaluation Account, Partner’s Capital Accounts and Balance Sheet)

Question 69 to 73 (Adjustments of the Old Partner’s Capitals on the Basis of New or Incoming Partner’s Capital)

Question 74 to 76 (When the New Partner is required to bring Proportionate Capital)

Question 77 to 78 (When New Partner has to bring Capital on the basis of Combined Capitals of Old Partners)