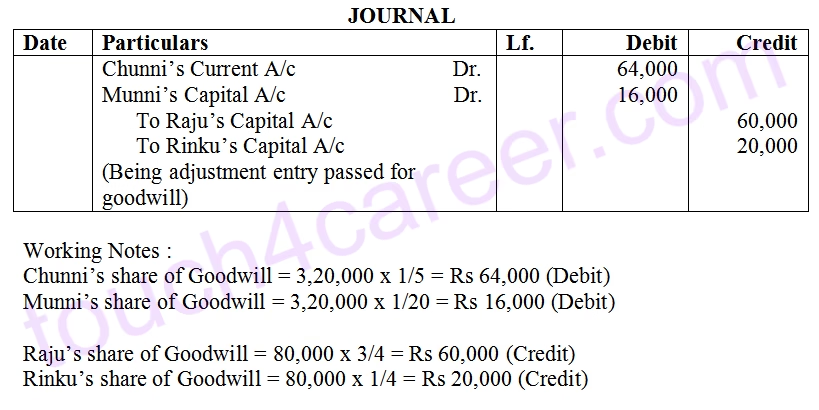

17. Raju, Rinku and Munni were partners sharing Profits & Losses in the ratio 3:1:1. They admitted Chunni into partnership for 1/5 share. It was decided that Munni will have 1/4 share in future profits. Goodwill of the firm was valued at Rs 3,20,000 and Chunni was unable to bring anything. Calculate New Ratio, Sacrificing Ratio and journalise for goodwill at the time of admission of Chunni.

Solution :-

Let total share be 1 Chunni share = 1/5

Remaining share = 4/5

Munni share = 1/4

Remaining share = 4/5 – 1/4 = 11/20

Raju share = 11/20 x 3/4 = 33/80

Rinku share = 11/20 x 1/4 = 11/80

New Ratio = 33/80 : 11/80 : 1/4 : 1/5 = 33 : 11 : 20 : 16

Sacrificing Ratio = 3 : 1 (Raju and Rinku)

Gain to Munni = 1/20