69 :- X and Y were partners in the profit sharing ratio of 3:2. Their balance sheet as at 31st March 2022, was as follows

Z was admitted for 1/6th share on the following terms

(i) Z will bring Rs 56,000 as his share capital, but was not able to bring any amount to compensate the sacrificing partners.

(ii) Goodwill of the firm is valued at Rs 84,000

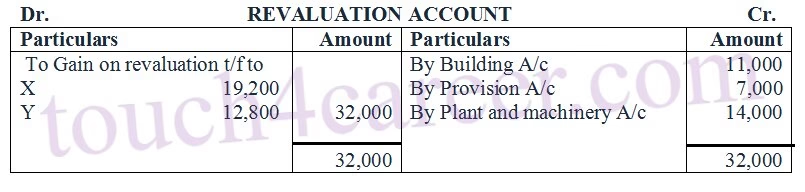

(iii) Plant and machinery were found to be undervalued by Rs 14,000 building was to be brought upto Rs 1,09,000.

(iv) All debtors are good.

(v) Capitals of X and Y will be adjusted on the basis of Z’s share and adjustments will be done by opening necessary current accounts.

You are required to prepare Revaluation Account and Partner’s Capital Accounts.

Solution :-

WORKING NOTES :-

(i) Calculation of goodwill’s share

Z’s share of goodwill = 84,000 x 1/6 = Rs 14,000

X’s share of goodwill = Rs 8,400

Y’s share of goodwill = Rs 5,600

(ii) Calculation of their new profit sharing ratio

X’s new share = 3/5 – 3/30 = 15/30

Y’s new share = 2/5 — 2/30 = 10/30

Z’s share = 1/6 x 5/5 = 5/30

New profit sharing ratio of X, Y and Z is 3:2:1

(iii) Adjustment of capitals

Total capital of the firm = 56,000 x 6 = Rs 3,36,000

X’s new capital = 3,36,000 x 3/6 = Rs 1,68,000

Y’s new capital = 3,36,000 x 2/6 = Rs 1,12,000