Get Exam-Ready with Class 12 Accountancy Sample Paper Solutions!

Struggling with tricky questions in your Accountancy sample papers? Don’t worry! At Touch4Career.com, we provide detailed and accurate solutions to all the questions of CBSE Class 12 Accountancy sample papers – fully aligned with the latest syllabus and marking scheme. Whether you’re revising for board exams or brushing up your concepts, our step-by-step explanations will help you score high with confidence.

Part A :- Accounting for Partnership Firms and Companies

1. A partner’s capital account was credited with Rs 80,000 during the year. Which of the following can be the possibility for such a credit in his capital account?

A.Opening Balance B. Drawings during the year

B.Loss during the year D. Capital introduced

OR

Assertion (A) :- Fluctuating Capital Account can show debit balance.

Reason (R) :- Losses and Drawings can be more than Capital Balance.

A.Both A and R are correct and R is the correct explanation of A

B.Both A and R are correct but R is not the correct explanation of A

C.A is correct but R is incorrect

D.Both A and R are incorrect

2.On 1st July, 2024, A, B and C entered into partnership sharing Profits & Losses in the ratio 5:3:2. C was guaranteed that his share of profits will not be less than Rs 60,000 p.a. Deficiency if any will be borne by A and B equally. For the year ended March 31, 2025, firm incurred loss of Rs 1,25,000. Deficiency will be borne by A and B will be:

A. A Rs 30,000 and B Rs 30,000 B. A Rs 43,750 and B Rs 26,250 C. A Rs 42,500 and B Rs 42,500 D. A Rs 35,000 and B Rs 35,000

3. Pali Limited offered 2,00,000 shares of Rs 10 each at a premium of Rs 2 per share. Applications were received for 1,95,000 shares, which were duly allotted. The amount was payable as Rs 3 on Application (including Rs 1 premium), Rs 6 on Allotment (including Rs 1 premium) and balance on call. Manoj, holding 6,000 shares failed to pay allotment money and his shares were immediately forfeited. Out of the forfeited shares, 4,000 shares were re-issued @ Rs 11 per share as fully paid up. The amount of Capital Reserve will be:

A.Rs 16,000 B. Rs 12,000 C. Rs 8,000 D. Rs 18,000

OR

Prafful Limited forfeited 15,000 shares of Rs 20 each on which Rs 8 (including Rs 2 premium) was paid. Out of these 13,000 shares were re-issued @ Rs 19 per share as fully paid up. Determine the amount of Share Forfeited balance.

A.Rs 90,000 B. Rs 91,000 C. Rs 12,000 D. Rs 16,000

4. Pista Ltd. took over running business of Vista Ltd. comprising of Assets of Rs 45,00,000 and Liabilities of Rs 7,50,000 and in consideration issued them 30,000, 9% debentures of Rs 100 each at 5% discount and a cheque of Rs 10,00,000. Determine the amount of Goodwill or Capital Reserve.

A.Goodwill Rs 9,00,000 B. Capital Reserve Rs 9,00,000 C. Goodwill Rs 1,00,000 D. Capital Reserve Rs 1,00,000

OR

Dawn Ltd. purchased Equipment and paid Rs 2,20,000 by cheque and issued 16,000 equity shares of Rs 10 each at 25% premium. The purchase consideration will be:

A. Rs 3,40,000 B. Rs 4,20,000 C. Rs 3,80,000 D. Rs 2,00,000

5. Bala and Lala were partners in a firm with Capitals of Rs 24,00,000 and Rs 16,00,000. They admitted Mala as a new partner for 1/3 share for which Mala brings Rs 20,00,000 as capital. There was Investment and Investment Fluctuation Reserve appearing in the books of Rs 2,50,000 and Rs 50,000 respectively. Bala took over 40% of the Investments at Rs 80,000 and remaining Investments were valued at Rs 1,10,000. By what amount Revaluation account will be affected for the above information?

A.Debited Rs 60,000 B. Credited with Rs 60,000 C. Debited Rs 10,000 D. Credited Rs 10,000

6. Jai and Veeru were in a partnership sharing Profit &Loss in the ratio 5:3. Their Capitals were Rs 10,00,000 and Rs 8,00,000 respectively. The firm was also having reserves of Rs 7,00,000. Normal rate of return was 10%. Firm made average profits of Rs 2,30,000 for the year ended March 31, 2025 (after adjustment of loss of machinery of book value of Rs 2,00,000 by fire against which insurance claim of Rs 1,50,000 was admitted). Value of goodwill as per Capitalisation of super profits will be:

A.Rs 10,00,000 B. Rs 3,00,000 C. Rs 18,00,000 D. Nil.

7. On 1st August, 2024 Tom, Jerry and Tyke entered into partnership with capitals of Rs 5,00,000 each. Interest on Drawings was to be charged @ 6% p.a. For the year ended March 31, 2025, Tyke withdrew Rs 80,000. What amount of Interest on drawings will be charged from Tyke?

A.Rs 4,800 B. Rs 1,600 C. Rs 3,200 D. Rs 2,400

8. A, B and C were partners sharing Profits &Losses in the ratio 7:2:1. B died. A took over 1/20 from his share and remaining share was taken over by C. Determine the new Profit sharing Ratio.

A. 4 : 1 B. 7 : 1 C. 71 : 29 D. 3 : 1

OR

X, Y and Z were partners sharing Profit & Losses in the ratio 5:3:2. Y retired, and he gifted half of his share to X and remaining half was taken over equally by X and Z. Determine the new Profit-sharing Ratio.

A. 29 : 11 B. 13 : 7 C. 1 : 1 D. 5 : 2

9. X, a partner was assigned to look after the dissolution process and was allowed remuneration of Rs 15,000. Actual realisation expenses amounted to Rs 20,000, being paid by another partner Y. By what amount Realisation account will be debited for the above-mentioned information?

A. Rs 20,000 B. Rs 35,000 C. Rs 5,000 D. Rs 15,000

10. Arun and Barun were partners sharing Profits &Losses in the ratio 3:2. They admitted Charan into partnership for 20% share. Charan was to bring proportionate Capital and he brought Rs 3,50,000 (including Rs 50,000 for goodwill share) in firm. If adjusted capital of Arun after Revaluation Gain/Loss, Accumulated Profits/Losses and Goodwill treatment was Rs 8,40,000. What was Barun’s Capital after Revaluation Gain/Loss, Accumulated Profits/Losses and Goodwill treatment?

A. Rs 5,60,000 B. Rs 3,60,000 C. Rs 12,00,000 D. Rs 6,60,000

OR

Raghav and Sahil were partners sharing Profit &Loss in the ratio 5:3. Their capital balances were Rs 7,20,000 and Rs 2,80,000 respectively. There were balances of General Reserve of Rs 5,00,000 and Deferred Revenue Expenditure of Rs 4,00,000 in the books of the firm. They admitted Ojasv into partnership for 20% share for which he brings Rs 4,00,000 as capital. Determine the goodwill share of Ojasv.

A. Rs 5,00,000 B. Rs 1,00,000 C. Rs 1,20,000 D. Rs 60,000

11. Building was appearing in the books at Rs 20,00,000 which was overvalued by 25%. What amount will be shown in the Balance Sheet of a reconstituted firm for building?

A. Rs 25,00,000 B. Rs 16,00,000 C. Rs 24,00,000 D. Rs 15,00,000

From the given hypothetical situation, answer Q 12 – 14.

Floater Ltd. issued 60,000; 8% debentures of Rs 100 each at 5% Discount and to be redeemed at 10% premium at the end of 5 years. On the date of issue, balance in Securities Premium was Rs 8,00,000 and Statement of Profit Loss (Dr.) was Rs 5,00,000.

12. Loss on Issue of Debentures is to be written off as _ out of Securities Premium and _) out of Statement of Profit and Loss.

A. Rs 4,50,000 ; Rs 4,50,000 B. Rs 6,00,000 ; Rs 3,00,000 C. Rs 8,00,000 ; Rs 1,00,000 D. Rs 4,00,000 ; Rs 5,00,000

13. After writing off Loss on Issue of Debentures, balance in Statement of Profit and Loss will be _

A.Debit ; Rs 6,00,000 B. Credit ; Rs 6,00,000 C. Debit ; Rs 4,00,000 D. Credit ; Rs 4,00,000

14. Premium on Redemption of Debentures account will have a balance of________ to be treated as __ in the first year.

A.Rs 9,00,000 ; Non-Current Liabilities B. Rs 9,00,000 ; Current Liabilities C. Rs 6,00,000 ; Non-Current Liabilities D. Rs 6,00,00 ; Current Liabilities

15. Arun, Basu and Tarun were partners sharing Profit &Loss in the ratio 5:3:2. Their firm was dissolved on March 31, 2025. On this date following assets and liabilities were appearing in their books of accounts.

Building Rs 2,00,000 ; Furniture Rs 80,000 ; Stock Rs 70,000 ; Goodwill Rs 10,000 ; Debtors Rs 40,000 ; Cash Rs 20,000 ; Creditors Rs 50,000 ; Arun’s Loan Rs 60,000 ; Tarun’s Brother Loan Rs 30,000. Assets realised at for Rs 3,40,000. Determine the amount of Realisation Gain/Loss.

A. Realisation Loss Rs 80,000 B. Realisation Gain Rs 60,000 C. Realisation Loss Rs 60,000 D. No Gain or Loss on Realisation

16. John and Sourabh were partners sharing Profit &Loss equally. They decided to share future Profit &Loss in the ratio 3:2. Their manager Arya met with an accident in the office itself and his claim for compensation amounted to Rs 50,000. The firm had a Workmen Compensation Reserve of Rs 80,000. Which of the following statement holds true at the time of reconstitution?

A. Rs 50,000 will be provided as workmen claim out of Workmen Compensation Reserve and balance Rs 30,000 will be distributed amongst partners in old ratio.

B. Rs 50,000 will be provided as workmen claim out of Workmen Compensation Reserve and balance Rs 30,000 will be distributed amongst partners in new ratio.

C. Rs 50,000 will be provided as workmen claim out of Workmen Compensation Reserve and balance Rs 30,000 will be credited to Revaluation Account.

D. Rs 50,000 will be provided as workmen claim out of Workmen Compensation Reserve and balance Rs 30,000 will be carried forward in the books of the firm without any treatment.

17. Raju, Rinku and Munni were partners sharing Profits & Losses in the ratio 3:1:1. They admitted Chunni into partnership for 1/5 share. It was decided that Munni will have 1/4 share in future profits. Goodwill of the firm was valued at Rs 3,20,000 and Chunni was unable to bring anything. Calculate New Ratio, Sacrificing Ratio and journalise for goodwill at the time of admission of Chunni.

OR

Yashasvi, Nitish and Harshit were partners sharing Profit &Loss in the ratio 5:3:2. W.e.f 01 April, 2025, they decided to share future Profit &Loss in the ratio 4:3:2. On the date of reconstitution Goodwill was appearing in the books of Rs 4,00,000. Goodwill of the firm was valued at Rs 7,20,000 on the date of reconstitution. Determine gain or sacrifice for each partner and pass necessary entries.

18. Hemant and Pankaj were partners sharing Profit & Loss in the ratio of 3:2. The firm was dissolved on March 31, 2024 and the following balances were appearing in the books of the firm.

a. Hemant’s Loan Rs 80,000

b. Ruby’s Loan Rs 50,000

c. Creditors Rs 1,00,000

d. Capital Balances after all adjustments – Hemant Rs 1,60,000 and Pankaj – Rs 1,40,000

Assets of the firm realised at Rs 6,00,000. You are required to show the amounts and order of payments as per section 48 of Indian Partnership Act 1932 at the time of Dissolution of the firm.

19. On January 01, 2025 Ritu Ltd. Issued Rs 40,00,000, 8% Debentures of Rs 100 each at 5% discount to be redeemed at 10% premium at the end of 5 years. Balance in Securities Premium on the date of such issue was of Rs 2,70,000. Pass entries for Issue of debentures.

20. Ankur and Vikram were partners sharing Profits & Losses in the ratio 3:2. They decided to share future Profits & Losses equally. On the date of reconstitution there was Investment Fluctuation Reserve of Rs 4,00,000 in the books of accounts. Pass entries in the following cases

A.Value of Investment reduced by Rs 2,50,000.

B.Value of Investment increased by Rs 5,00,000.

C.There was no change in value of investments.

21. Sapphire Ltd. Was registered with an authorised capital of Rs 80,00,000 divided into 4,00,000 shares of Rs 20 each. Company offered and issued 1,50,000 shares at a premium of Rs 4 per share payable as Rs 7 on application (including Rs 1 premium), Rs 12 on allotment (including Rs 2 premium) and balance on first call. Rancho, holding 10,000 shares failed to pay allotment and call money. Another shareholder Sultan holding 5,000 shares failed to pay the call money. All the shares held by Rancho were forfeited and of these 8,000 were reissued at Rs 22 per share as fully paid.

Show Share Capital sub head as it would in the Balance Sheet of Sapphire ltd. along with notes to Account as per the Companies Act 2013.

22. Amit, Sumit and Pulkit were partners sharing Profit &Loss in the ratio 5:3:2. Their Capitals were Rs 8,00,000; Rs 7,00,000 and Rs 5,00,000 respectively. According to Partnership Deed:-

(a) Interest on Capital @ 10% p.a.

(b) Salary to Amit Rs 10,000 p.m and Pulkit Rs 15,000 per quarter.

(c) Commission to Sumit Rs 70,000.

(d) Sumit was being guaranteed that his share of profits will not be less than Rs 65,000. Deficiency if any will be borne by Amit and Pulkit equally.

Ignoring the above terms the profits of Rs 6,00,000, for the year ended March 31, 2025 were divided equally between partners. You are required to pass necessary adjustment entry. Show your workings clearly.

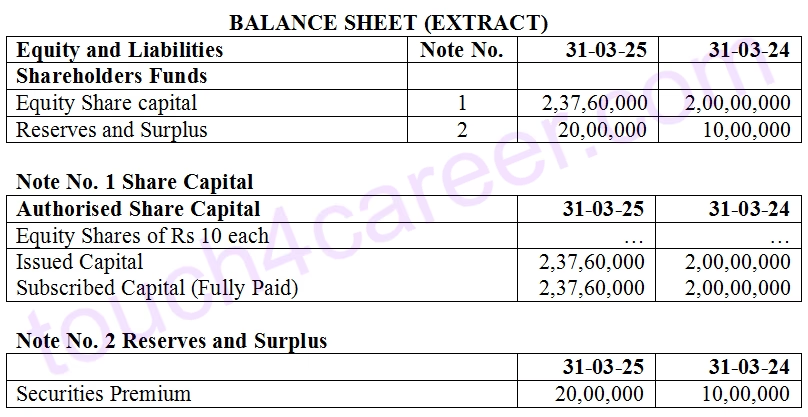

23. Extract of Financial statements of Alexa Ltd are produced below.

During the year Alexa ltd. purchased business of Gloria ltd. with assets of Rs.50,00,000 and liabilities of Rs.20,00,000. With regards to the following additional Information:

1) During the year 40,000 Equity Shares were issued at a premium of Rs.4 per share for cash.

2) Besides this no shares were issued as sweat equity, bonus or as ESOP or in any other form.

Give journal entries for issue of shares for cash and consideration other than cash. Also, prepare Share Capital A/c and Securities Premium Account in the books of Alexa ltd.

24. Alok, Deepak and Manish were partners sharing Profit &Loss in the ratio 5:3:2. pak retired on March 31, 2025. On this date his dues after all adjustments related to Revaluation Gain/Loss, Accumulated Profits/Losses and Goodwill treatment came out to be Rs 6,40,000. He was paid Rs 40,000 through Furniture on retirement and it was agreed to pay balance in three equal annual instalments together with interest as per the rate permissible by act, in the absence of any agreement. First instalment being paid on March 31, 2026. You are required to pass entry for immediate payment to Deepak on retirement and prepare Deepak’s Loan Account till it is finally closed.

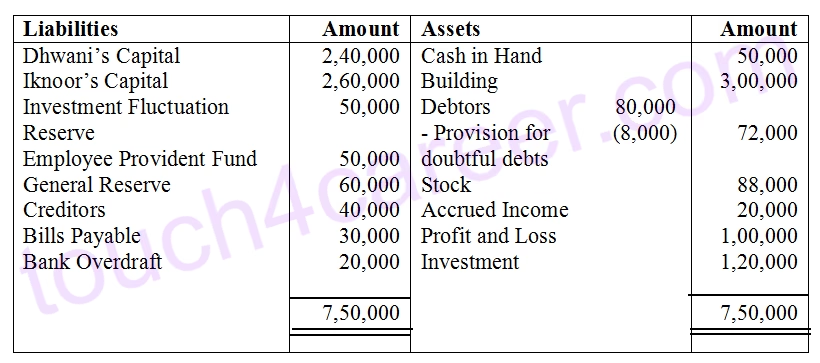

25. Dhwani and Iknoor were partners sharing Profits & Losses in the ratio 3:2. Their Balance Sheet on March 31, 2025 was as follows

On the above date, they admitted Ishaya into partnership for 25% share. Ishaya brings Rs 2,50,000 as capital and Rs 40,000 for goodwill. Goodwill of the firm was valued at Rs 2,00,000. Following agreements were agreed upon:-

a) Bad Debts amounted to Rs 5,000 and Provision for doubtful debts to be created at same existing rate.

b) Investments were valued at Rs 1,00,000.

c) Accrued Income was recovered only of Rs 14,500 in settlement.

d) Building was overvalued by 20%.

e) Capital of Dhwani and Iknoor were to be adjusted on the basis Ishaya’s capital contribution. Necessary adjustment to be done by opening Current Accounts.

You are required to prepare Revaluation Account and Partner’s Capital Account at the time of admission of partner.

OR

Aman, Barman and Raman were partners sharing Profits & Losses in the ratio 5:3:2. Their Balance Sheet on March 31, 2025 was as follows

On the above date Barman retired and his share was acquired by Aman and Raman equally. Following agreements were agreed upon:-

a) Create Provision for doubtful debts @ 10%.

b) Market value of Building is Rs 1,00,000 and Furniture was overvalued by 20%.

c) Stock was valued at Rs 55,000. Creditors of Rs 15,000 took over stock of Rs 10,000 in settlement of their claims.

d) Goodwill of the firm was valued at Rs 80,000.

e) Prepaid Expenses are worthless and Outstanding Expenses are now Rs 20,000.

f) Rs 20,000 was immediately paid to Barman on retirement brought in Aman and Raman in ratio 3:2.

Prepare Revaluation Account and Partner’s Capital Account at the time of retirement of partner.

26. Space Ventures Limited was registered with an authorised capital of Rs 20,00,000 divided into 2,00,000 shares of Rs 10 each. The company offered 80,000 shares for public subscription payable Rs 4 on application and Rs 7 on allotment (including Rs 1 premium). Public had applied for 1,10,000 shares and pro-rata allotment was made in the ratio of 5:4. Remaining applications were rejected. Mukta, holding 6,000 shares failed to pay allotment money. Her shares were being forfeited and later re-issued 4,000 shares at a discount of Rs 2 per share. Pass necessary entries in the books of Space Ventures Ltd.

OR

Chitinoor Ltd. invited applications for 2,00,000 shares of Rs 10 each payable Rs 3 on application, Rs 5 on allotment (including Rs 1 premium) and balance on call. Applications were received for 3,00,000 shares out of which 20% applications were rejected and remaining were allotted on pro-rata basis. Rohan, an applicant of 12,000 shares failed to pay allotment money and Mohan holding 8,000 shares paid the entire money along with allotment. Subsequently the call was made, all the money was duly received except from Rohan. Later on, company issued a notice to Rohan to pay the balance in 15 days failing which his shares would be forfeited. Rohan cleared his dues within the stipulated time period. Journalise.

Part B :- Analysis of Financial Statements

(Option – I)

27. A company had following balances in their books of Accounts

Determine the amount of Change in Inventories to be shown in Statement of Profit and Loss Account.

A. Rs 20,000 B. Rs (20,000) C. Rs (10,000) D. Rs 10,000

28. Inventory Turnover Ratio of company was 5 times. The firm had Revenue from operations of Rs 5,00,000 and Gross Profit was 25% of Cost of Revenue from Operations. Determine the amount of Opening Inventory if Closing Inventory was Rs 60,000.

A. Rs 80,000 B. Rs 60,000 C. Rs 1,00,000 D. Rs 50,000

OR

Assertion (A) :- Gross Profit Ratio is always higher than Net Profit Ratio.

Reason (R) :- To calculate Net Profit, Indirect Expenses are subtracted from Gross Profit and Indirect Incomes are added to Gross Profit.

A. Both A and R are correct, and R is the correct explanation of A

B. Both A and R are correct, but R is not the correct explanation of A

C. A is correct but R is incorrect

D. A is incorrect but R is correct

29. Proposed Dividend for the year ended March 31, 2025 and March 31, 2024 were Rs 2,50,000 and Rs 2,00,000 respectively. Shareholders finalised the dividend amount at Rs 1,80,000 during the year ended March 31, 2025 in AGM held in June-July 2024. Unclaimed dividend as at March 31, 2025 was Rs 10,000.

Choose the correct option while preparing Cash Flow Statement for the year ended March 31, 2025:

A. Proposed Dividend added in Net Profit after tax will be Rs 2,00,000 and outflow of Dividend paid in financing activities will be Rs 1,90,000.

B. Proposed Dividend added in Net Profit after tax will be Rs 2,50,000 and outflow of Dividend paid in financing activities will be Rs 2,00,000.

C. Proposed Dividend added in Net Profit after tax will be Rs 1,80,000 and outflow of Dividend paid in financing activities will be Rs 1,90,000.

D. Proposed Dividend added in Net Profit after tax will be Rs 1,80,000 and outflow of Dividend paid in financing activities will be Rs 1,70,000.

OR

Provision for Tax for the year ended March 31, 2025 and 31 March 2024 were Rs 3,00,000 and Rs 2,80,000 respectively. During the year Tax paid was Rs 2,50,000. Determine the amount of Tax proposed during the year by the firm.

A. Rs 3,00,000 B. Rs 2,30,000 C. Rs 2,80,000 D. Rs 2,70,000

30. Which of the following is cash flow from Operating activities for a finance company:

A. Conversion of debentures into shares B. Dividend received C. Building purchased D. Dividend paid

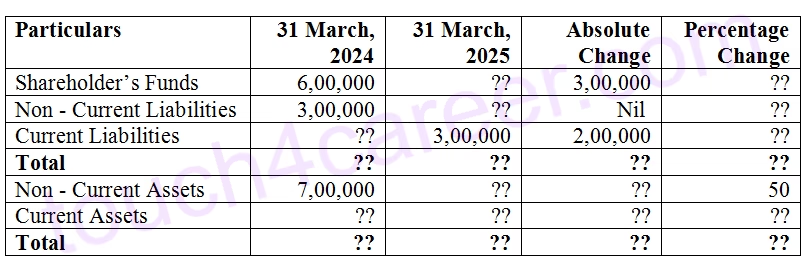

31. Complete the following Comparative Balance Sheet as at March 31, 2024 and Match 31, 2025

OR

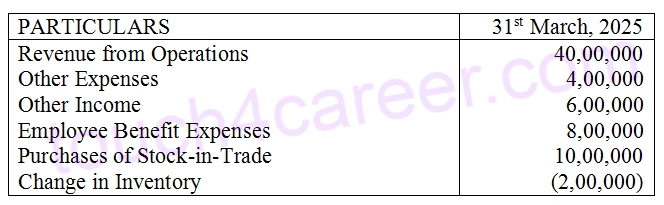

Prepare Common Size Statement of Profit and Loss for the year ended March 31, 2025.

Tax Rate 50%

32.

(i) Give two examples of Inventory except Raw Materials, Work in Progress, Finished Goods and Stock in Trade.

(ii) Where will you disclose the amount of loss on issue of debentures written off out of Statement of Profit and Loss?

(iii)Where will you disclose Purchase of Raw Materials in Financial Statement of Company?

33. Quick Ratio of Roxy Traders is 0.8 : 1. State with reasons whether the following transactions will increase , decrease or will have no change on the ratio.

a) Goods purchased on Credit

b) Outstanding Expenses paid

c) Sale of Fixed Assets a 20% loss

d) Issue of Debentures at Premium to Vendors

OR

From the following information, calculate Trade Receivables Turnover Ratio: Cost of Revenue from Operations (Cost of Goods Sold) : Rs. 6,00,000 Gross Profit on Cost : 25% Cash Sales: 20% of Total Sales Opening Debtors: Rs. 1,00,000 Closing Debtors : Rs. 2,00,000. Provision for Doubtful Debts: Opening Rs. 10,000 and Closing Rs.20,000.

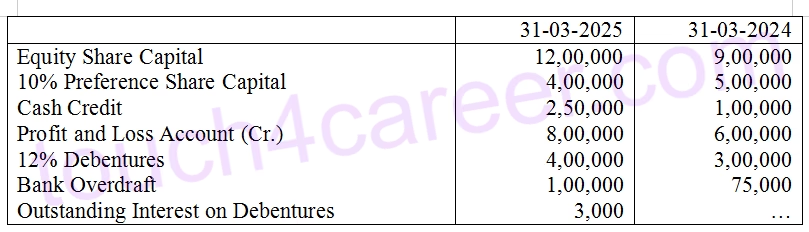

34. Extracts of the Balance Sheets of M/s Agrawal Ltd. as on 31st March,2024 and 31st March 2025 along with additional information are given below. You are required to calculate:

(i) Operating profit before changes in working capital.

(ii) Cash Flows from Financing Activities.

Additional Information:

a) New equity shares and debentures were issued on last day the current accounting year ended 31st March, 2025. Debentures were issued at a discount of 5% which was written off at the end of the year.

b) Dividend on preference shares and interim dividend @ 15% were paid on equity shares on 31st March, 2025

c) Preference Shares were redeemed on 1st April, 2025 at a premium of 5%. The premium was provided out of profits